Retail Media Radar – May 2026: Retail Media moves from expansion to execution

Over the past few months, Radar has explored the infrastructure emerging underneath retail media and AI-driven commerce: agentic systems, machine-readable discovery, payment rails and the growing role of data in automated decision-making. What May's signals show is something more practical.

The conversation is shifting away from possibility and towards implementation. Retailers are deploying AI inside stores against specific operational problems. Measurement frameworks are becoming more rigorous. Retail Media Networks are moving closer to the workflows and standards that brand budgets already expect. And physical retail is being reassessed as a measurable commercial environment with distinct advantages of its own.

A few developments this month make that shift particularly visible.

Kroger and YouTube: SKU-level conversion reporting

Kroger Precision Marketing has integrated with Google’s Display & Video 360 to let brands see SKU-level sales results from YouTube campaigns for the first time. It connects ads to actual purchases from around 60 million loyal households.

Built using LiveRamp and MetaRouter (which securely move customer data into marketing tools without third-party tracking), it works with no extra setup for brands already using DV360.

Key benefits:

Brands can target Kroger shopper audiences on YouTube and see exactly which products (down to SKU level) were sold from ads.

Campaigns can be optimised in near real time based on actual sales, not delayed or indirect metrics.

In-store tracking across 2,700+ Kroger stores is coming next.

The key shift is that retail media can now combine strong brand advertising (like YouTube) with direct proof of sales impact. Because it sits inside DV360, it also removes a lot of friction that has previously limited brand investment in retail media.

More broadly, the real advantage in retail media sits in the quality and depth of purchase data, with formats and reach as the means of activating it rather than the source of leverage itself.

Find out more here.

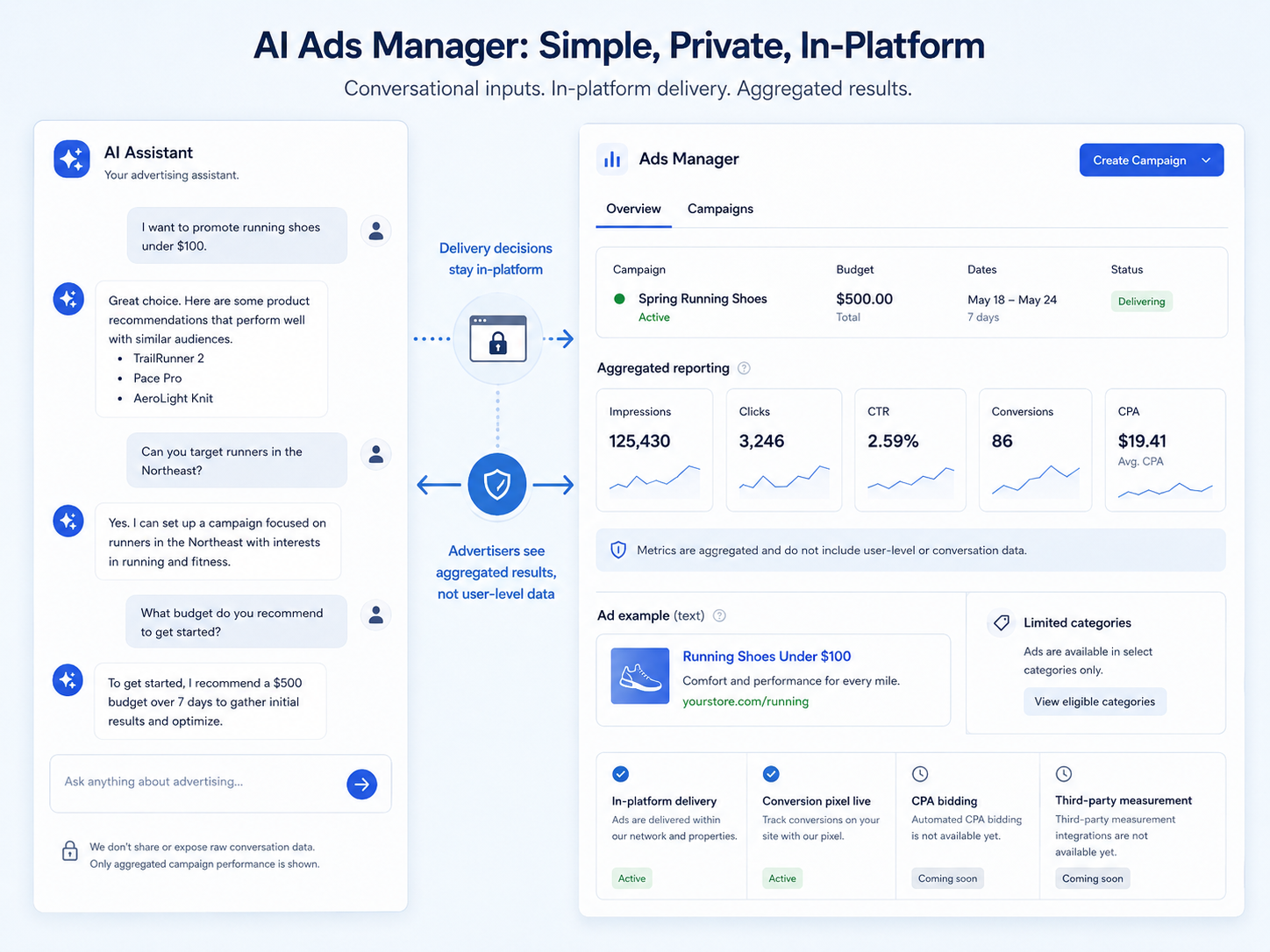

ChatGPT opens its ads manager: what it means for retail media

OpenAI has opened its ChatGPT ads manager to all US advertisers, removing the previous $50,000 minimum spend threshold. Cost-per-action bidding and third-party measurement are confirmed as forthcoming, with a conversion tracking pixel already live.

Campaign delivery decisions remain entirely within OpenAI's own system.

Advertisers receive aggregated performance data, not the underlying conversation signals.

Ad formats remain deliberately lightweight, protecting the user experience and neutrality of responses.

Eligible categories remain limited while moderation and compliance infrastructure matures.

The more important question is whether conversational intent carries the same commercial value as retail intent. Someone asking ChatGPT for recommendations is demonstrating interest, not necessarily proximity to purchase.

OpenAI's choice to keep delivery in-house reflects an understanding that its commercial value depends on the credibility of its outputs. Any advertising model built around AI recommendations relies on users continuing to trust those recommendations. That constraint will shape how aggressively monetisation expands from here.

For retail media practitioners, the more useful frame may be to think of ChatGPT advertising as a consideration channel rather than a conversion one - complementary to retail media rather than competing with it, at least for now. The interesting planning question is how the two work in sequence, not which one wins.

Find out more here.

Measurement as competitive advantage: Best Buy and the accountability shift

Best Buy Ads is making measurement a core part of its advertising offer, not something simply added afterwards.

It is building a unified system that combines multi-touch attribution with geo-based studies to link store visits and sales back to advertising.

For brands that sell products in Best Buy (endemic brands), the focus is on SKU-level sales impact. For others, it measures things like reach and consideration instead.

It is working with Circana and Kantar to create a full view of performance across all channels, not just individual ads.

Best Buy is also being open that in-store measurement is still evolving, and it is prioritising getting consistent standards right over moving quickly.

The bigger point is that measurement consistency is becoming a competitive advantage. Retailers that can prove impact clearly are likely to earn more trust and longer-term budget commitments, while those that don’t risk losing spend over time.

Find out more here.

Proprietary AI agents and the battle for customer relationship ownership

Alibaba is integrating its Qwen AI with Taobao, its main e-commerce platform, to let shoppers search, compare and buy products through a conversational interface across more than 4 billion listings.

Qwen AI is Alibaba’s in-house large language model family. It powers chat-based assistants that can understand natural language, recommend products, answer questions and support decision-making.

Taobao is Alibaba’s core consumer marketplace, where billions of products are listed and purchased, with logistics, payments and after-sales services all built into the same ecosystem.

The integration means shoppers can now browse and purchase directly through conversation, with logistics and post-purchase services embedded in the same flow. Importantly, the AI is not a standalone tool - it sits directly on top of Alibaba’s own commerce infrastructure (catalogue, pricing, fulfilment and service), keeping the entire transaction inside one system.

Key implications:

Conversational browsing and purchasing keep more of the shopper journey inside Alibaba’s ecosystem, strengthening its understanding of how users search, compare and convert.

Features like virtual try-ons and price tracking suggest this is aimed at supporting the full shopping journey, not just improving search.

Similar AI commerce strategies are emerging elsewhere, including Google’s work with retailers like Kroger, Lowe’s and Papa Johns on Gemini-powered agents, as well as in-house assistants like Walmart’s Sparky and Lowe’s Mylow.

The broader strategic risk is that if discovery and comparison move into third-party AI assistants, retailers may be reduced to fulfilment layers rather than owning the customer relationship. In response, many are building their own AI agents to retain control of the shopping interface.

This is also a data strategy. Every interaction inside a retailer’s own AI system generates behavioural signals that remain within its ecosystem. If those interactions happen inside external AI platforms, that data is lost - and over time, that difference in data ownership could become a major competitive advantage or disadvantage.

Find out more here.

AI in the physical store: moving from pilot to practice

Across UK retail, AI deployment in physical stores has been building quietly and is now starting to show up in concrete, operational ways.

Iceland has deployed AI-driven replenishment tools that analyse demand data in real time, factoring in seasonal peaks, promotions and trading anomalies.

Tesco is trialling an AI assistant tested with 280,000 employees, focused on meal planning and basket building ahead of a customer rollout.

Morrisons has introduced Google's Gemini to help shoppers locate products in store using natural language search against each store's specific inventory.

M&S has equipped 11,000 store managers with Microsoft 365 Copilot to free up time for customer-facing activity.

Sainsbury's has built Nectar360 Pollen, a unified retail media platform bringing audience insights, planning, activation, optimisation and multi-touch attribution into one portal.

LVMH has built a data and AI platform across 75 maisons, including a client advisor tool at Tiffany & Co that surfaces customer preferences in real time.

In each case, AI is being applied to a specific operational problem rather than deployed as a general capability in search of a use case. That distinction matters because it changes how the investment is justified and how success is measured.

Of all the developments in this group, Sainsbury's/Nectar 360 Pollen is the one worth watching most closely. When audience insights, campaign activation and measurement sit within a single infrastructure, the relationship between media spend and sales becomes easier to interrogate - and AI is being used to change what the store contributes commercially, rather than simply how it operates. The others deliver real efficiency value. Pollen is attempting something structurally different. Physical retail is being equipped to perform better at the things it has always been best placed to do.

Find out more here.

May's signals point to a market where the questions being asked are becoming more specific. What is emerging is a more practical set of demands: does the measurement hold up, can brand budgets be justified, does AI inside the store actually improve commercial performance, and who controls the customer relationship when AI intermediates commerce?

What retains value across all of this is proof - that the audience is right, that the signal is clean and that the methodology stands up to scrutiny. That requires governance and aligned ownership across retail, media, loyalty and technology, something many organisations are still working to operationalise.

One pattern worth watching is whether measurement rigour and discovery strategy are being treated as the same problem or sequential ones. The networks investing in both simultaneously are likely to be better positioned than those solving for accountability first and worrying about AI-mediated discovery later.

Physical retail is increasingly functioning as the operational centre of a connected retail media system - the place where inventory, media, loyalty and transaction data still sit within a single environment that retailers fully control. As digital discovery fragments across platforms, agents and external intermediaries, that level of integration becomes commercially valuable in a different way.